Often young professionals find themselves in the tough spot of not having enough credit established, or having a low credit score.

Despite responsible spending, people just starting out in their careers still face challenges that are not faced by other age brackets.

Young people are often faced with multiple different forms of debt at the same time.

The combination of paying off student loans, making car payments, along with typical everyday living costs, add up quickly.

Especially added to credit card debt, often with extremely high interest rates, these payments can cause many problems.

However, it is reasonable to manage these debts if you focus on these four major ways to refinance various costs.

1. Student Loans

Surprisingly, student loans can be refinanced if needed, with relative ease.

Even established professionals have issues with student loans because they follow you for years.

It is one of the most prominent debt issues in our society.

The average college graduate deals with nearly $30,000 of debt on average.

Some of these loans, such as PLUS loans, can carry a very high interest rate.

Refinancing this debt to attain lower interest rates can be a huge benefit, especially if you think it will take you many years to pay off the debt.

Multiple different private lenders work with refinancing student debt.

2. Car Loans

If you took out an auto loan post-graduation, you may end up paying interest rates as high as almost 5%.

A common misconception is that car loans are fixed interest.

This is simply not true.

Car loans can be refinanced relatively easily.

Many different private lenders provide this service.

If you have fantastic credit, you may be able to refinance your car loan interest to as low a rate as 1% in some cases.

2% interest rates are also attainable in many instances.

You need a good credit history along with proof of timely payments over the course of several years.

If this is the case, then refinancing can save you a lot of money, especially since cars take a long to pay off sometimes.

You can also refinance your loan through credit unions.

These are typically able to offer even lower rates than you would be able to find at any dealership.

3. Mortgages

Refinancing your mortgage is one of the best ways to save money and pay off debt faster.

Mortgage rates are at a relative low.

You can lower your rate or change your monthly payments in order to meet new interest rates after refinancing.

It is important to think about how your credit, good or bad, may affect the terms of a mortgage refinance plan.

It will be difficult to secure a better interest rate if you have demonstrably poor credit.

The closing costs on a mortgage can be very high, so it’s important to sit down and do the math to figure out if you really would save money in the long term, even with a lower interest rate.

It is best not to extend your repayment term because this additional time may offset the benefits of a lower interest rate.

If you are experiencing financial difficulty and need to extend the time in order to stay in your home, then do so.

Otherwise, it is best to steer clear of this path.

4. Credit Cards

As evidenced in the graph below, credit card interest rates fluctuate wildly month by month, and on the whole, they have been rising over time.

Even though this can be inconvenient, it also opens up possibilities for refinancing your credit card debt at a lower interest rate.

This August, the average annual interest rate on credit card debt was above an incredible 15%.

Those with high credit card debt find that with such a high premium, it can be nearly impossible to pay this down, even while making regular payments since the interest adds up drastically.

The best way to avoid this is to keep on the lookout for credit card offers so you can transfer your balance and pay off your card at a lower interest rate.

Sites like NerdWallet can help compare different offers from around the web and help you see which ones you qualify for.

However, to qualify for these, you need good or great credit, usually meaning a score that is above 680.

This plan makes sense if you can pay off your debt quickly, otherwise, it just racks up more credit card issues in the long term.

Over time, you will accumulate debt and have the same issues.

Usually, credit card companies require you to pay a fee for transferring your balance.

That means it is only worthwhile if you can pay off your debt within the promotional period.

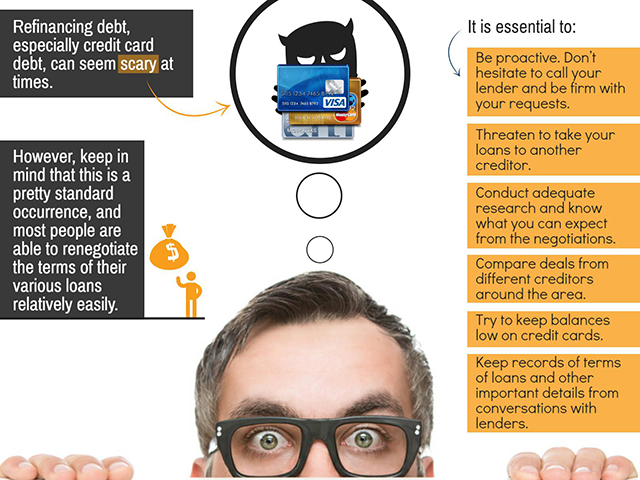

Additional Tips

These tips will help you get started in negotiating your debt.

If you take it one step at a time, you will be able to renegotiate successfully and save yourself lots of money down the line.

Chapter 11 bankruptcy isn't uncommon, yet many fail to see its purpose. Most people have…

Applying for personal loans after a bankruptcy discharge? Getting approved may not be easy, but…

Student loan wage garnishment is the last thing you want to experience while paying student…

Here's what happened on Financial Wellness 1. How to Start Investing in Stocks Even With…

Trashing your credit score is so much easier than building a solid credit rating. It's…

Does debt consolidation hurt your credit or not? Consolidating your debt sounds like a good…

{kind=link}

{kind=link}