Sometimes taking out loans or other lines of credit can be more of an investment than debt in the long run.

This especially applies to certain types of debt, like student loans.

But at the end of the day, debt is debt, and you’ll have to pay it back sooner or later.

This is why you need to be smart about how much you borrow, as well as what you’re borrowing for.

It’s all too easy to find yourself in debt and not know how you got there.

Here are a few general tips to avoid falling into the debt trap (see a complete list here):

Now that you know how to better avoid debt, let’s look at what you shouldn’t swipe that credit card for:

That getaway to the Bahamas is going to cost you a pretty penny.

While the shore and sunshine may be calling your name, it’s best not to listen unless you’ve saved up a significant sum for your vacation fund.

Taking out a new line of credit for your trip will almost definitely cause you even more stress in the long run.

(More stress will mean you’ll need another vacation, starting to see the pattern here?)

You never know what kind of financial mishap could be waiting for you when you come home, so you’ll want to be prepared.

This one will go hand in hand with avoiding the temptation of sales.

While you might need a new work shirt or new athletic shoes, don’t go overboard with retail therapy.

It’s important that you don’t charge more to a card than you can afford to pay off in a month.

The same principle applies when you’re buying anything, not just clothes or shoes.

But it’s especially important when it comes to shopping trips.

What’s the point in looking fashionable if you’re broke?

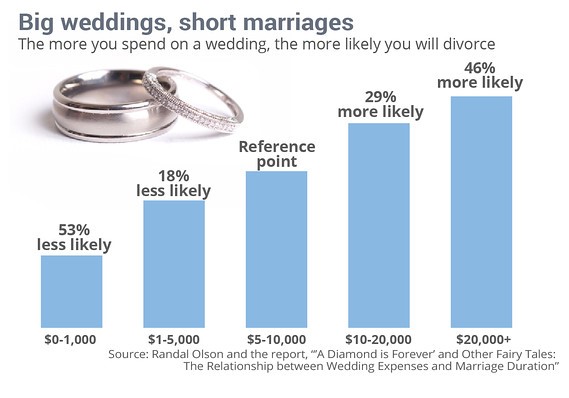

Many of us have dreamed of a lavish wedding to a beautiful princess or handsome prince charming.

But, no matter how much you might love your soon-to-be spouse, you won’t want to max out that credit card to pay for your walk down the aisle.

Weddings can be expensive, there’s no doubt about that.

One in eight Americans spends more than $40,000 on their “I do”.

Remember, marriage is about the lifelong connection that you’re trying to establish with your spouse, not the glitz and glamour of a ceremony that lasts less than a day.

Smartphones have become a staple in our lives.

They help us stay organized; they keep us in touch with important people, and they help us relax after a tough day at work.

But let’s face it – the biggest names in tech are conning us just a little bit.

You might think the latest iPhone is worth that $600, but Apple is likely already set to release a new one next year.

Tech is constantly changing, faster than consumers can keep up.

So don’t try, unless you can afford it with your hard earned cash.

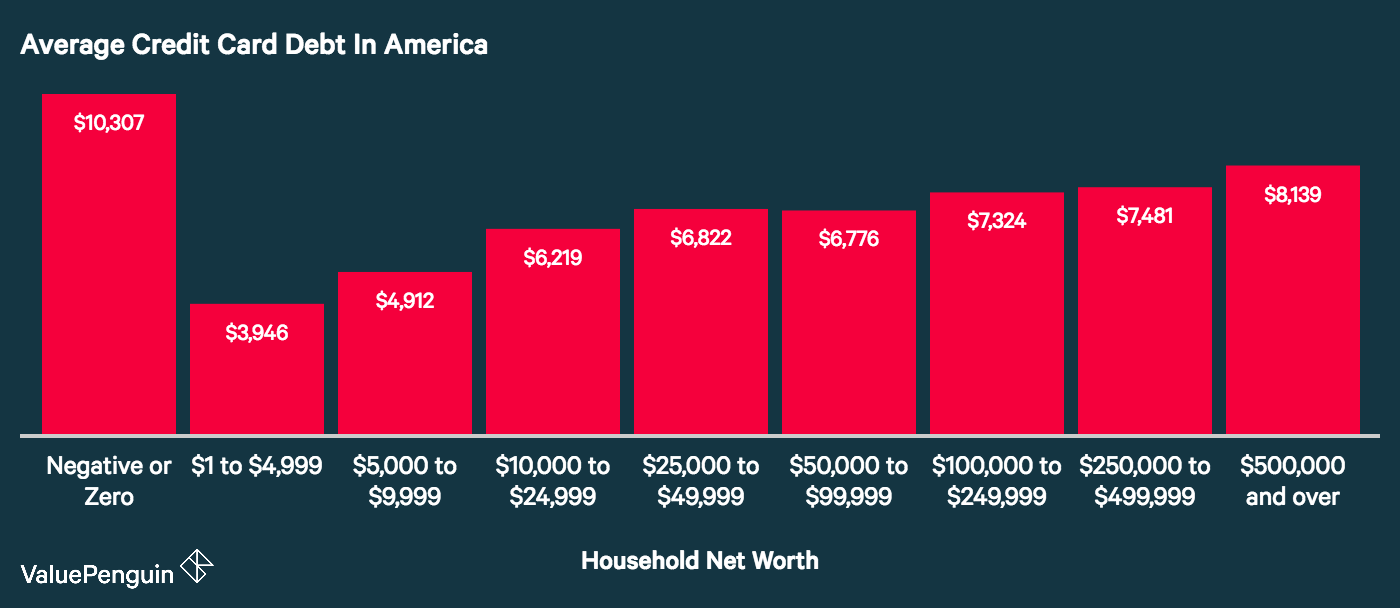

After looking at the chart below, is it really worth going into credit card debt for a new gadget?

The main takeaway is that you should save going into debt for the big, important stuff in life – buying a house or a car, taking out student loans, or keeping a credit card for emergencies.

It’s a good idea to make small purchases on your card that you can quickly pay off each month so you can maintain a good credit score.

However, a little foresight goes a long way.

Make sure you’re swiping that credit card for good reasons, and not accruing massive amounts of debt for fleeting extravagances.

Chapter 11 bankruptcy isn't uncommon, yet many fail to see its purpose. Most people have…

Applying for personal loans after a bankruptcy discharge? Getting approved may not be easy, but…

Student loan wage garnishment is the last thing you want to experience while paying student…

Here's what happened on Financial Wellness 1. How to Start Investing in Stocks Even With…

Trashing your credit score is so much easier than building a solid credit rating. It's…

Does debt consolidation hurt your credit or not? Consolidating your debt sounds like a good…

{kind=link}

{kind=link}

{kind=link}