It is important to make certain financial considerations before getting married.

It is true that financial concerns are one of the number one reasons for divorce.

Couples should communicate their concerns before the wedding, and take measures to ensure that they are financially sound.

A couple in the U.S. did what many couples do in the lead up to their wedding.

For 14 months, they concentrated on choosing the venue and other details.

The chart below shows the breakdown of expenses:

However, they also found time to consult a financial adviser.

They raised issues such as opening joint accounts or staying financially independent.

They also considered upcoming life events and how they will save for them.

Unfortunately, many couples avoid discussing money matters before tying the knot.

They believe it will cause friction when they want it to be a time of enjoyment.

This is a mistake, and you should make time for honest talks about money.

You can use the past to make future decisions in your life as a married couple.

Write down your individual goals and concerns, share them with your partner and then listen to him/her.

One partner may be planning on early retirement.

This would mean spending less and start saving for the future.

Each partner should compile a net-worth statement.

This will show a more accurate picture of the total financial position you each have.

It will also allow you to start discussions about how to manage certain issues such as paying off a debt.

You might decide to have joint accounts for certain purposes.

These could be for things like paying household bills or saving to buy a home.

You might make the decision to share liability for expenses or, alternatively, divide up expenses.

Generally, it might be advisable not to share debt.

Individual debt such as college fees should remain separate.

Possibly the only common debt should be a mortgage.

In this way, you are protected against reckless actions by your spouse, and your individual credit score is protected.

It might be difficult to make ends meet at the beginning of a marriage.

Young people might be just starting their careers.

It is essential to plan a budget and stick to it which will prevent overspending and credit card debt.

As a newlywed, you should draw up certain legal documents:

You don’t have to cancel your student loan debt or credit cards.

However, you should work on keeping your debts manageable.

Figure out how much you’re able to pay on them, and when you will have the balances at zero.

Put some cash away for a rainy day.

Saving money could be a blessing should either of you lose your job or have work hours reduced.

In today’s economy, this is essential.

Take out insurance policies.

This will cover you for issues like a car accident or house damage.

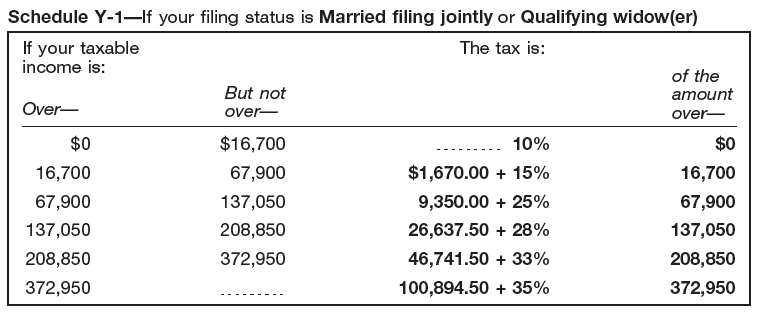

The tax code penalizes married couples whose combined income is between $200,000 and $300,000.

The marriage penalty changes into a marriage benefit if one partner isn’t earning a lot of money.

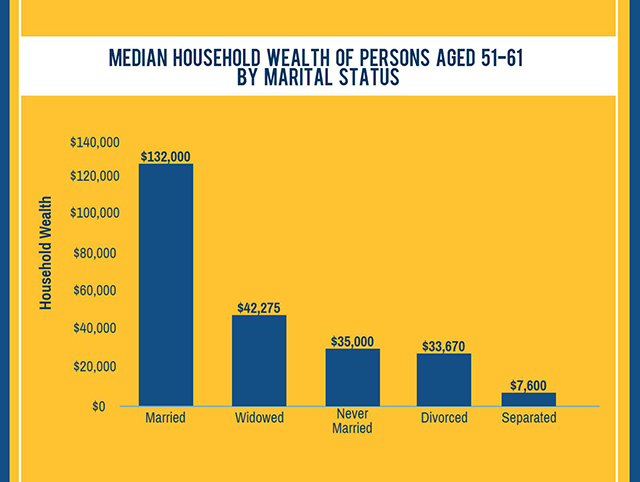

The chart below demonstrates the household prosperity for seniors in the range of marital status.

It would seem that it is financially viable to stay together as a married couple.

If you are a widower or widow before 60, who has remarried, you will lose survivor benefits.

These have been founded on the deceased spouse’s income.

If you divorce or your spouse dies, you are eligible to apply for benefits.

Remarriage will mean that alimony payments will cease unless the divorce decree states otherwise.

It is possible that you will also lose pension benefits from the deceased spouse.

As well other survivor benefits, annuities of firefighters and police officers could also cease.

One downside to marriage is the possibility it will affect your children’s entitlement to college financial aid.

The Free Application for Federal Student Aid takes into account the assets and income of both spouses.

This applies if only one is the child’s parent.

On the plus side, if both parents have children, getting married would increase the size of the household.

If there is an increase in the number of children in college, eligibility for financial aid could also increase.

Older couples might reject marriage when considering the high cost of health care.

This is particularly true of long-term care.

After marriage, you take on responsibility for your spouse’s medical bills.

Your partner having to go to a nursing room would mean your estate is reduced.

The issue is that Medicare does not cover most care.

Also, combined assets are taken into account when you are considered for Medicaid.

Financial problems such as unemployment and adversity can have detrimental affects on your marriage.

This will be the case if you cease communicating with one another and avoid facing the issues.

You need to talk and acknowledge the money concerns.

Short term unemployment can stretch out to long-term unemployment.

Added to this, unemployment benefits may be terminated.

If this happens to you or your spouse, feelings of depression, panic and blame may set in.

It will be beneficial to find ways to cope with the stress that appeals to both of you.

It is important to talk about the situation you find yourselves in.

Place the focus on what you can do and attempt to do it.

Learning to work as a team will strengthen your relationship.

You need to be realistic.

You can consider your fixed expenses and flexible expenses.

Pinpoint where you can cut back such as deciding not to eat out or living without cable or satellite television.

Also, think about a vegetable garden, working odd jobs, or opening your own small business.

It is essential that you control spending.

Only use credit cards for emergencies or health care.

Try not to use your savings unless you reach a consensus that the expense is absolutely vital.

Seek help and don’t let your ego or pride prevent you from getting assistance.

You may be entitled for help in receiving:

Do your homework about your legal rights when it comes to your debts.

Don’t try and escape from the unemployment and financial issues.

By overeating, smoking, drinking, over-spending, and not sleeping, you are making your position worse.

It is essential you look after yourself both physically and emotionally.

A newlywed couple started to discuss their financial situation.

They found out they were $52,000 in debt.

This was comprised by $18,000 in car loans, $7,000 in credit card debts, and $27,000 in student loans.

The Phoenix couple paid it off over the next 18 months by:

They had received a wake-up call and decided to act immediately.

They made the decision to merge their finances when they got married.

After writing down all the data, they discovered how serious the situation was.

Before writing everything down all in one place they hadn’t realized that they needed to do something to change things.

They examined their finances once a month and used the ‘debt snowball’.

This meant paying off a small debt first and being able to feel that they were achieving something.

It psychologically helped to increase momentum.

Reducing every service they owned helped.

These included cable, cell phone, and insurance.

The husband canceled gym membership, they ate in more often, and didn’t order drinks when eating out.

These measures allowed them to put extra cash into the debt.

They admitted to feeling overwhelmed.

They had moved on from being single in their own homes to joining two households.

She had started her career, and he had commenced a new job; the financial circumstances added to the stress.

Their financial goal was to be totally debt-free in five years.

This would mean paying off car loans, credit cards, and student loans, to name a few.

By their mid-thirties, they plan to be totally debt-free, including their mortgage.

This couple’s story is an incentive for everyone to get their finances under control.

Whether unemployment has struck, or over-spending has been an issue, there are ways of dealing with a financial crisis.

Many couples make the choice not to wed because of financial concerns.

Good communication and a plan of action can help the situation.

Chapter 11 bankruptcy isn't uncommon, yet many fail to see its purpose. Most people have…

Applying for personal loans after a bankruptcy discharge? Getting approved may not be easy, but…

Student loan wage garnishment is the last thing you want to experience while paying student…

Here's what happened on Financial Wellness 1. How to Start Investing in Stocks Even With…

Trashing your credit score is so much easier than building a solid credit rating. It's…

Does debt consolidation hurt your credit or not? Consolidating your debt sounds like a good…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}