Confused about where to start when it comes to your finances? Don’t worry, most of us don’t. But it’s important to take control of your financial life early on. Check out these 7 financial tips for millennials to get you headed in the right direction.

To see a real difference in your financial situation, you need to be aware and in control of where your money goes. Making a budget could be the single most important thing you can do with your finances.

Think about where you could make changes to save money. Do you need to go out for cocktails with friends, or could you have just as much fun at home with a bottle of wine? Small savings can add up.

As a millennial, you’re probably used to having an app for everything. So why not for your money? There are hundreds of apps and websites that will allow you to track your saving and spending and pay your bills all in one place.

Most can be used with a computer, phone, or tablets and will offer reminders and alerts, so you stay fully aware of your finances.

It’s a good idea to have some financial goals in mind. Whatever your goals are, you should make a plan that will help you to achieve them. Otherwise, they will stay as dreams instead of becoming a reality.

As well as making plans, you should also prepare for the worst with an emergency fund. If you can only save for one thing, make it your emergency fund, rather than your dream vacation.

It’s crucial for millennials to make sure they have plenty of funds set aside for retirement. There are several different types of retirement funds to choose from – find a full list here. The most common of these are:

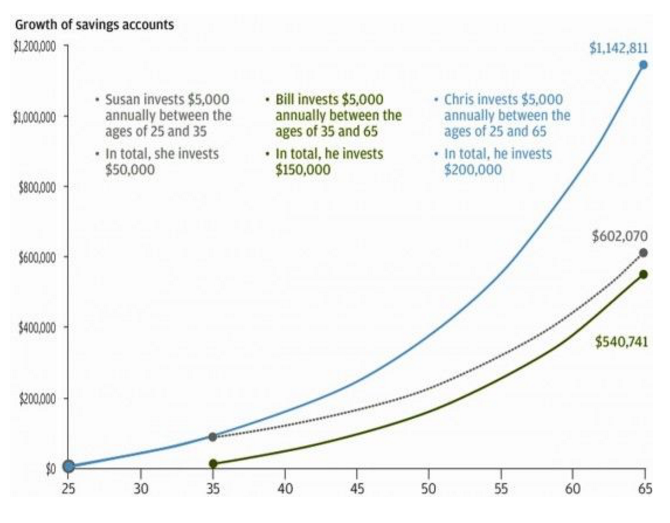

The chart below is based on a Roth IRA but shows how important it is for millennials to start paying into a retirement fund as early as possible.

Source: http://www.ourfreakingbudget.com/why-we-max-out-our-roth-ira/

If like many millennials, you’re new to investing, it could be a good idea to start trying it out. Find a reputable financial adviser, get a recommendation from someone you trust, and take their advice.

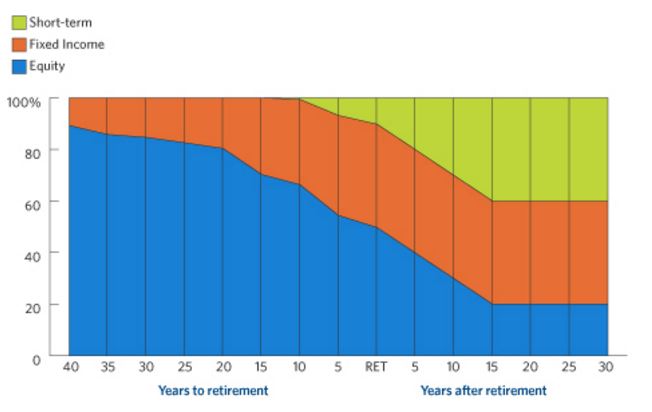

One way to get started is a target-date retirement fund. These offer a range of investments all in the same place and are designed to become more conservative as you approach retirement.

Source: https://www.ici.org/pubs/faqs/faqs_target_date

The graph gives an example of how assets in a target-date retirement fund may be allocated. Other examples can be found here.

Since millennials carry an average debt of $47,689, learning to handle debt well is an important thing. Some debts are positive, others less so.

Good debts are those with lower interest rates, often around 6-8% and include:

Bad debt has a higher interest rate and needs to be paid off quickly to avoid accumulating interest. Examples would be:

If you have the latter kind of debt, you can improve things by using extra funds to pay off the debt with the highest interest rate first and then moving on to the next highest and so on. Aim to pay your debt off as quickly as possible.

Your credit score affects so many aspects of your life that you can’t afford to neglect it. Make a point of checking your credit score each year and fixing any errors you find. If you don’t have one already, take out a credit card and use it regularly. Just make sure to pay your bills on time.

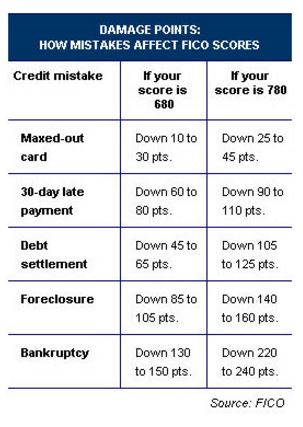

The table below shows the effect of a late payment on your credit score. The best way to avoid any problems is to set up an autopay on your credit card account, so you never miss a payment. If you can set it up to pay off the full balance, that’s the best. You don’t have to carry a balance over to improve your credit score.

You may not be able to do all these things immediately, but using even one of these tips will help you to improve your financial situation both now and in the future.

Chapter 11 bankruptcy isn't uncommon, yet many fail to see its purpose. Most people have…

Applying for personal loans after a bankruptcy discharge? Getting approved may not be easy, but…

Student loan wage garnishment is the last thing you want to experience while paying student…

Here's what happened on Financial Wellness 1. How to Start Investing in Stocks Even With…

Trashing your credit score is so much easier than building a solid credit rating. It's…

Does debt consolidation hurt your credit or not? Consolidating your debt sounds like a good…

{kind=link}

{kind=link}

{kind=link}