Are your finances spiraling out of control? Can’t see past your debt? If this situation sounds familiar, you may already have considered filing bankruptcy. We’ll explain to you when bankruptcy makes sense so you can figure out if it’s the right decision for you. Or, if you should explore other options of becoming debt free.

Bankruptcy is a legal system designed to help people who are too deep in debt to get themselves out. It’s a way for them to start fresh in relation their finances. There are two main types of bankruptcy for individuals.

Chapter 7 bankruptcy could be thought of as liquidation or ‘straight bankruptcy’. In this process, your non-exempt assets are sold off to pay off as much debt as possible. Any remaining debt is then written off.

Chapter 13 bankruptcy is often called a ‘reorganization bankruptcy’. It is based on your income and sets a structure to help you repay as much debt as possible in a 3-5 year time-frame. Any outstanding debts will then be written off.

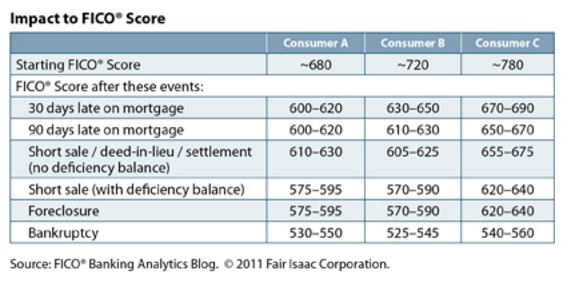

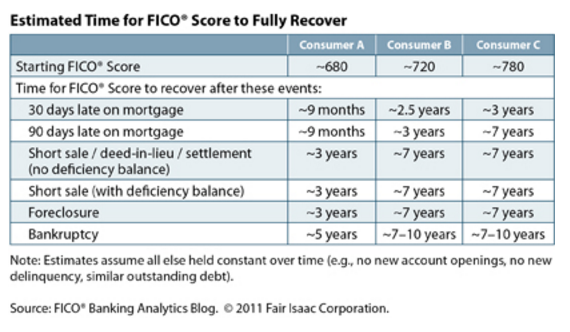

A major disadvantage of bankruptcy is its effect on your credit score. As shown in the tables below, your score will drop dramatically and stay low for a long time – usually 7-10 years. This means that it is vital to be certain that filing bankruptcy is the best option for you.

If you are thinking of filing bankruptcy, you need to be certain that things are as bad as you think. First, find out how much your assets are worth. Remember to count all stocks, bonds, retirement accounts, savings accounts, real estate, and retirement funds. Estimate the value of each and find a rough total figure for your assets.

Next, do the same for your debts, remembering to include all bills and credit statements.

Keep in mind that bankruptcy may not be the only way to solve your problems. Here are some situations where other options may be better.

Even if none of these situations apply to you, you may still be able to avoid declaring yourself bankrupt. Ask yourself these questions first.

In some situations, filing bankruptcy may be the best option. Warning signs might include:

In these circumstances, it could be a good idea to seek professional advice about declaring bankruptcy.

In conclusion, bankruptcy may seem like your only option, but there are things you can try before going down that route. It is worth exploring these because of the disadvantages associated with filing bankruptcy. You’ll have to deal with the effect on your credit score and the possibility of losing sentimental assets. However, if you have done your research and explored the other possibilities, then bankruptcy can be a useful way to press the reset button on your financial life.

Chapter 11 bankruptcy isn't uncommon, yet many fail to see its purpose. Most people have…

Applying for personal loans after a bankruptcy discharge? Getting approved may not be easy, but…

Student loan wage garnishment is the last thing you want to experience while paying student…

Here's what happened on Financial Wellness 1. How to Start Investing in Stocks Even With…

Trashing your credit score is so much easier than building a solid credit rating. It's…

Does debt consolidation hurt your credit or not? Consolidating your debt sounds like a good…

{kind=link}

{kind=link}