Most people know plenty of ways to save money.

They clip coupons, limit eating out, and might even restructure their mortgage.

Few, however, ever speak of refinancing their auto loan.

It may be a more reasonable option than you would think.

Compared to a house, refinancing a vehicle is relatively simple and easy.

First, let’s briefly cover in what situations you shouldn’t refinance.

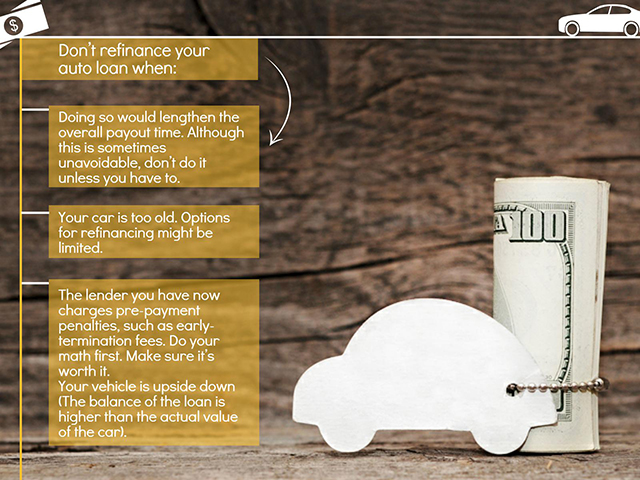

When Not to Refinance

Shown below are the situations in which refinancing your car wouldn’t be worthwhile.

So, what would make you consider the decision to refinance your car?

Read on to know the benefits you can derive out of refinancing.

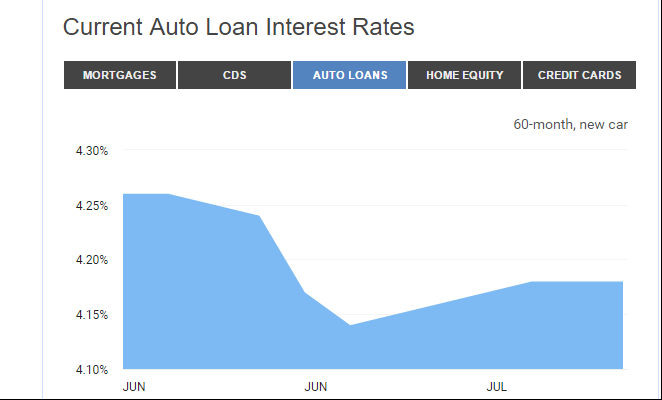

Interest Rates May Have Gone Down

Interest rates fluctuate over time.

Just look at the graph below.

It shows the average rate for a new car loan over the last three months.

As you can see, there was a big dip around late June.

Imagine the differences over three years.

Many assume that once they sign an auto loan contract, it can never be changed.

That is not the case.

If rates are lower than they were when you took out your loan, try for a better deal.

Even the smallest reduction in rate can make a huge difference in the long run.

Better rate means more savings!

You could get a better rate from another lender, or even from the one you have already.

Similarly, you can get a better rate simply by changing lenders.

Sometimes you can even get your current lender to lower theirs.

Changing lenders is very simple.

If you are approved, the old lender will give you money to pay off the old one.

This gives legal ownership of the car to the new lender.

In a sense, one lender is “buying” the car from the other.

You are the middle-man.

From then on, you’ll make payments to the new lender.

You can start making payments at the new interest rate.

If possible, however, you could continue with the old one.

You’ll pay off the loan faster and pay less interest overall.

Your Credit Score Has Gone Up

Along with Reasons 1 and 2, your credit score can help you get a better rate.

This applies if your score has increased since you first took out the loan.

You could get a lower rate based on the most recent score.

Your Income Has Improved

Are you making more money than you did when you took out your loan?

Perhaps you’ve gotten a better-paying job or promotion in the meantime?

That’s another reason to refinance.

You could convert a long-term loan into a short-term loan.

The result is, your monthly payments will be higher.

On the plus side, you’ll be done with it quicker and pay less interest.

You are facing financial burden

We all fall on hard times now and then.

If it’s difficult to make ends meet, refinancing your auto loan could help.

The effect is the opposite as that of refinancing for a higher income.

You will get a lower monthly payment in exchange for a longer term and higher interest.

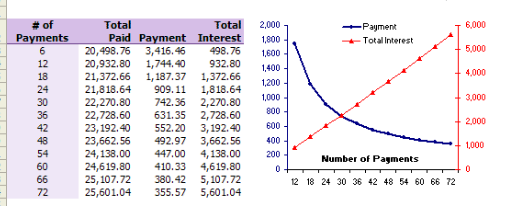

The graph below shows the relationship between the size of the payment and total interest rate.

But, this should be avoided if at all possible.

However, if you miss a payment or end up being late, that could hurt your credit score.

In that case, this is the lesser of two evils.

So stay updated and keep these points on hand!

Saving a few bucks through refinancing could really work out to your advantage!

Chapter 11 bankruptcy isn't uncommon, yet many fail to see its purpose. Most people have…

Applying for personal loans after a bankruptcy discharge? Getting approved may not be easy, but…

Student loan wage garnishment is the last thing you want to experience while paying student…

Here's what happened on Financial Wellness 1. How to Start Investing in Stocks Even With…

Trashing your credit score is so much easier than building a solid credit rating. It's…

Does debt consolidation hurt your credit or not? Consolidating your debt sounds like a good…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}